Welcome back to the first Digital Health Wire of 2026! The healthcare industry doesn’t take any days off, but we hope our readers managed to catch a break over the holidays to recharge for the big things to come in the new year.

The past few weeks have had plenty of fortune tellers predicting what those big things will be, so we’re kicking off the year with a compilation of the clearest crystal balls.

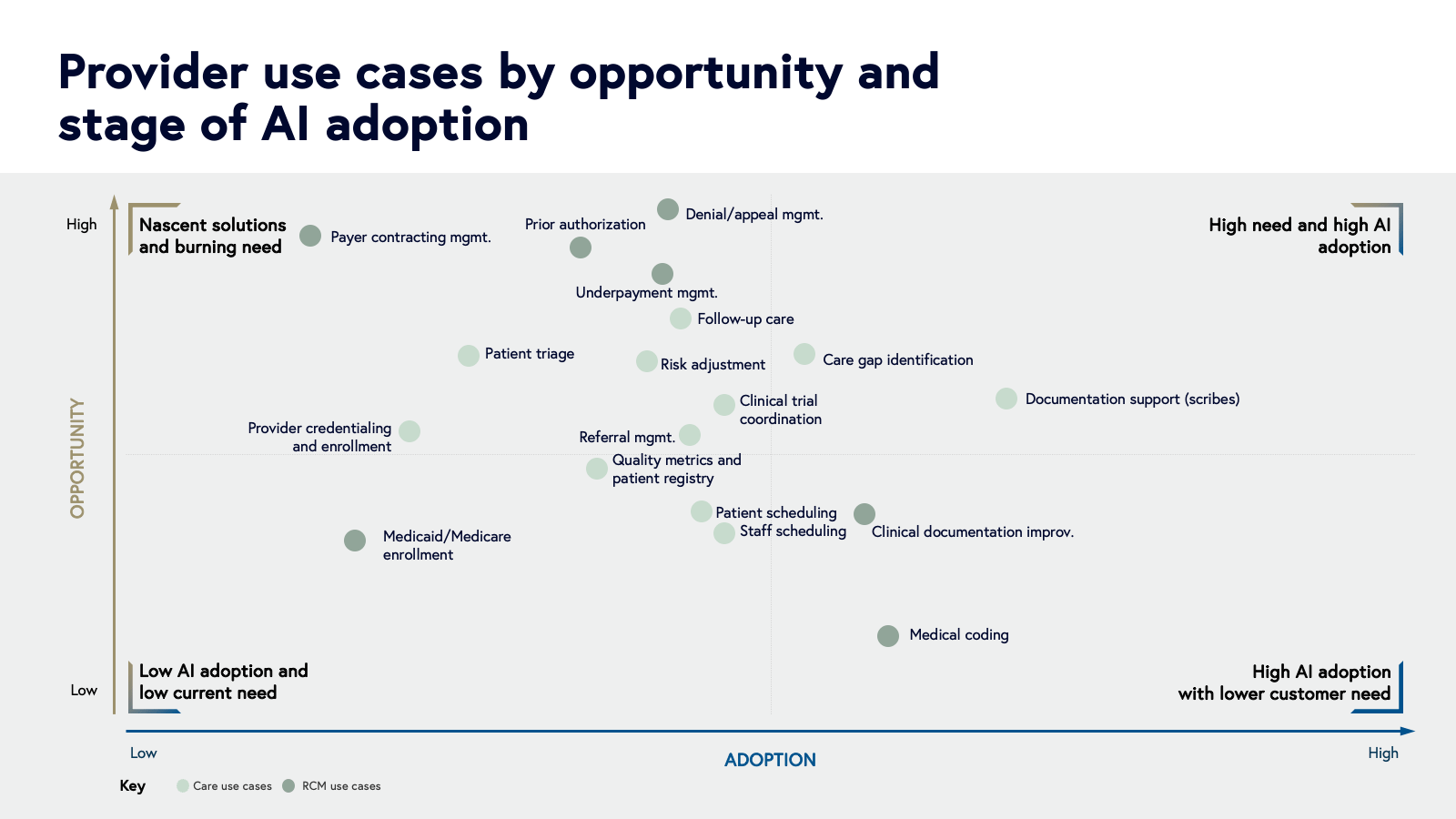

Let’s get right into it.

CommonSpirit Health – Five Health Tech Predictions for 2026, Dr. Minal Shah

- Favorite Forecast: In 2026, AI projects without strategic alignment are heading straight to the pilot graveyard. When organizations chase what’s possible instead of what’s strategic, they burn human capital on change efforts that never scale to real impact.

- Big Idea: “Platform vs. point solution is a false dichotomy – and I think we’re asking the wrong question. The real question isn’t which approach to take. It’s whether we’ve done the hard work of understanding what the organization actually needs before we choose a path forward. That means moving from ‘what can we do with AI?’ to ‘what should we be doing with AI?'”

Out-of-Pocket – Out-Of-Pocket’s 2026 Predictions, Nikhil Krishnan

- Favorite Forecast: Intellectual property lines will be drawn for AI. We’ve already seen a ton of legal battles around copyrights, but the dealmaking is just getting started.

- Big Idea: “Healthcare has a TON of companies that have copyrights and IP ownership over critical parts of healthcare information. OpenEvidence for example has signed several agreements with medical societies, NEJM, etc. Who will the AMA partner with for CPT codes? Which companies will the EHRs partner with to license their data?”

Second Opinion – Healthcare in 2026, Christina Farr & Annalisa Merelli

- Favorite Forecast: The largest digital health companies will start flocking to CMS’ new ACCESS program to find a better business model in Medicare, while also duking it out for a slice of the available rural health funding.

- Big Idea: “There’s no question digital health companies will be the beneficiaries, particularly given that the executive and policymaker running Medicare – Chris Klomp – has an entrepreneurial background and formerly sat on the board of venture-backed Maven Clinic.”

Becker’s – How the AI conversation will change in 2026, Zachary Lipton

- Favorite Forecast: Clinical decision support has been trapped in a frustrating middle zone for years: better than manually searching guidelines, but worse than talking to a specialist. CDS will finally start evolving beyond search with contextual awareness.

- Big Idea: “This is the year CDS evolves past glamorized search. Next-generation CDS will reason jointly over medical literature, the patient’s record and current visit context, helping clinicians apply knowledge, not just retrieve it.”

Forbes – 10 Healthcare Industry Predictions For 2026, Sachin Jain

- Favorite Forecast: Healthcare’s AI revolution will hit speed bumps. While AI has shown considerable promise for relatively straightforward uses like ambient dictation, its application in other domains will be more challenged and problematic.

- Big Idea: “Agentic AI holds significant promise, but legacy operators will be slow to change deeply ingrained processes, values, and attitudes. AI snake-oil salespeople (fueled by venture capitalists chasing outsized returns) have flooded the zone, a phenomenon that is sure to fuel false starts and threaten the pace and depth of true organizational change in the short-run.”

Hospitalogy – 8 Predictions for Healthcare 2026, Blake Madden

- Favorite Forecast: In 2026, enterprise buyers will start demanding consolidation. The operational model shifts from “best of breed for each use case” to “who can orchestrate AI across our entire administrative and clinical workflow?”

- Big Idea: “This is where the Palantir playbook becomes relevant. The firm is already working with HCA and others to deploy AI infrastructure that spans clinical, operational, and financial domains. The value proposition isn’t any single algorithm. It’s the orchestration layer that ties disparate data sources into unified decision support.”

Notable – Healthcare’s pivotal year for AI transformation, Dr. Aaron Neinstein

- Favorite Forecast: New practices will be built from scratch around AI Agents to support panel sizes three to five times larger at equal or higher quality and dramatically lower cost. At the same time, human connection will take center stage again.

- Big Idea: “AI will handle pattern analysis and routine adjustments, so clinicians can shift from memorizing facts to focusing on meaning… Because of this, nurses, MAs, and care coordinators will move up the value chain, as they can spend more time on empathy, clinical judgement, and complex situations rather than administrative tasks.”

The Takeaway

Healthcare still has its fair share of challenges, but it has just as many tailwinds pushing it toward new solutions. Cheers to everyone making those solutions a reality in the new year.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}