Of all the AI market overviews that have hit the wire recently, none have generated more buzz than Menlo Venture’s State of AI in Healthcare. One look at the report and it’s easy to see why.

First things first. Here’s a couple high-level callouts before we zoom in on the details:

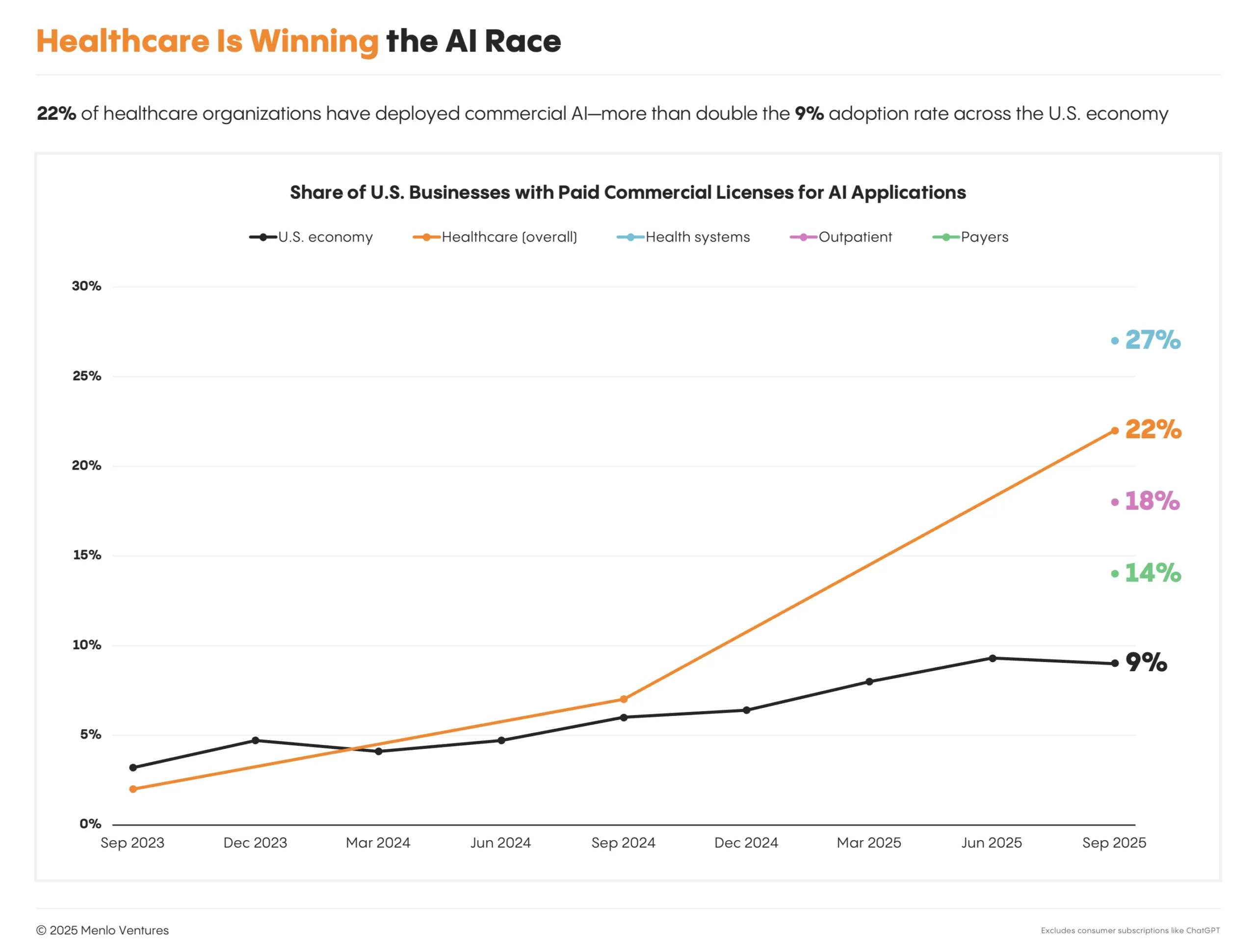

- Healthcare AI spending has already topped $1.4B in 2025 – 22% of healthcare orgs have now implemented domain-specific AI tools, a 7x increase over last year [Chart 1].

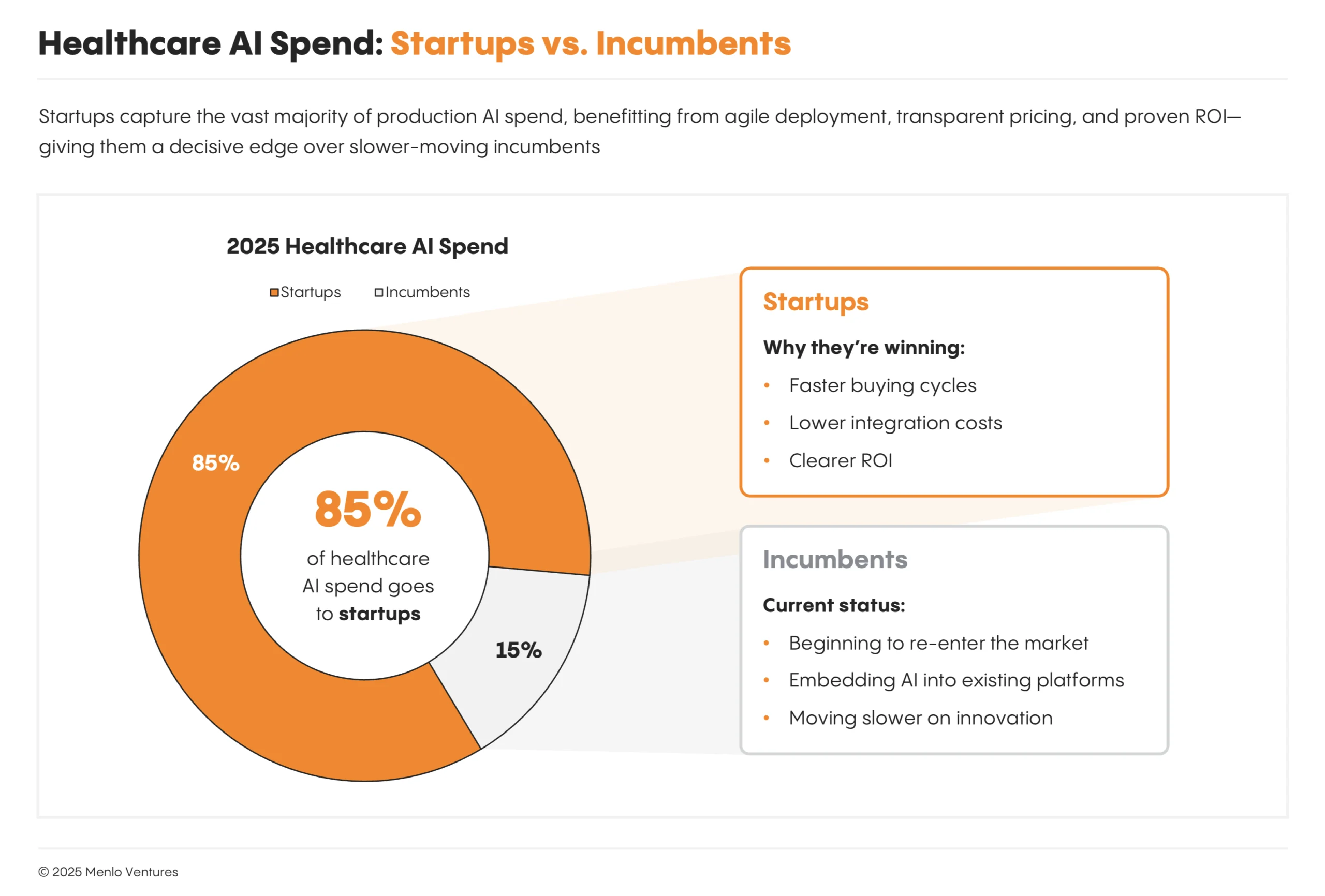

- 85% of all healthcare AI spend is currently flowing into startups (faster cycles, clearer ROI), rather than incumbents (often layering AI on legacy platforms) [Chart 2].

Providers accelerate, payors deliberate. Providers dominate AI adoption in healthcare, especially health systems – supplying $1B of the $1.4B total spending.

- Outpatient providers represent $280M, while payors surprisingly contribute just $50M.

The song remains the same. Menlo found that leading health systems are choosing AI based on themes we’ve covered plenty of times before. They prioritize:

- Tech maturity – providers prioritize production-ready solutions that perform at scale.

- Risk level – tools that don’t directly interface with patients see less scrutiny.

- Quick value – a 2025 favorite, rapid ROI and organizational confidence are essential.

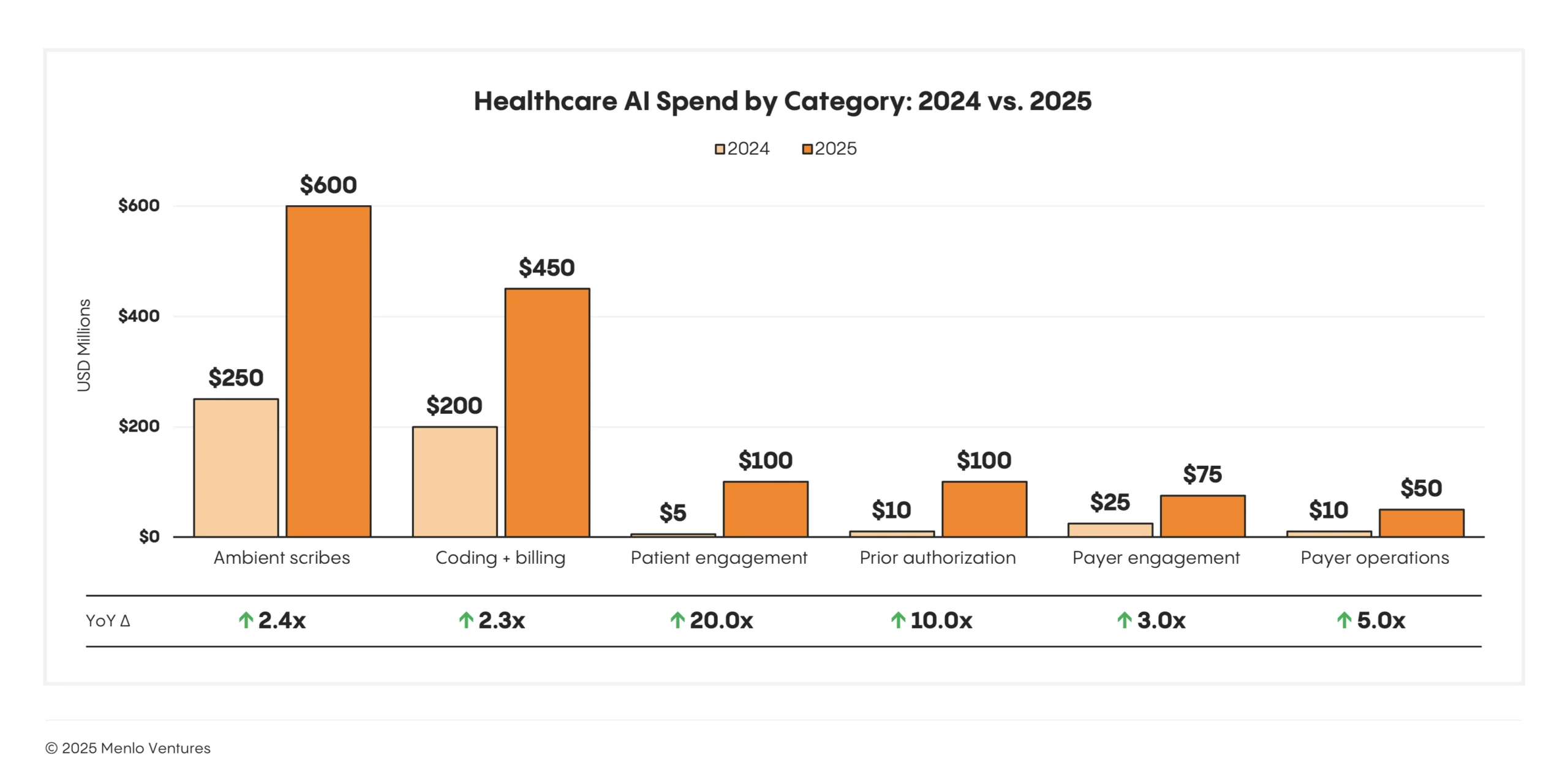

What solutions check all the boxes? Two categories account for the lion’s share of AI budgets, in large part because they quickly address acute operational pain points.

- Ambient documentation ($600M), no surprise here. This puts it in perspective [Chart 3].

- Coding and billing automation ($450M), hard to think of a quicker ROI.

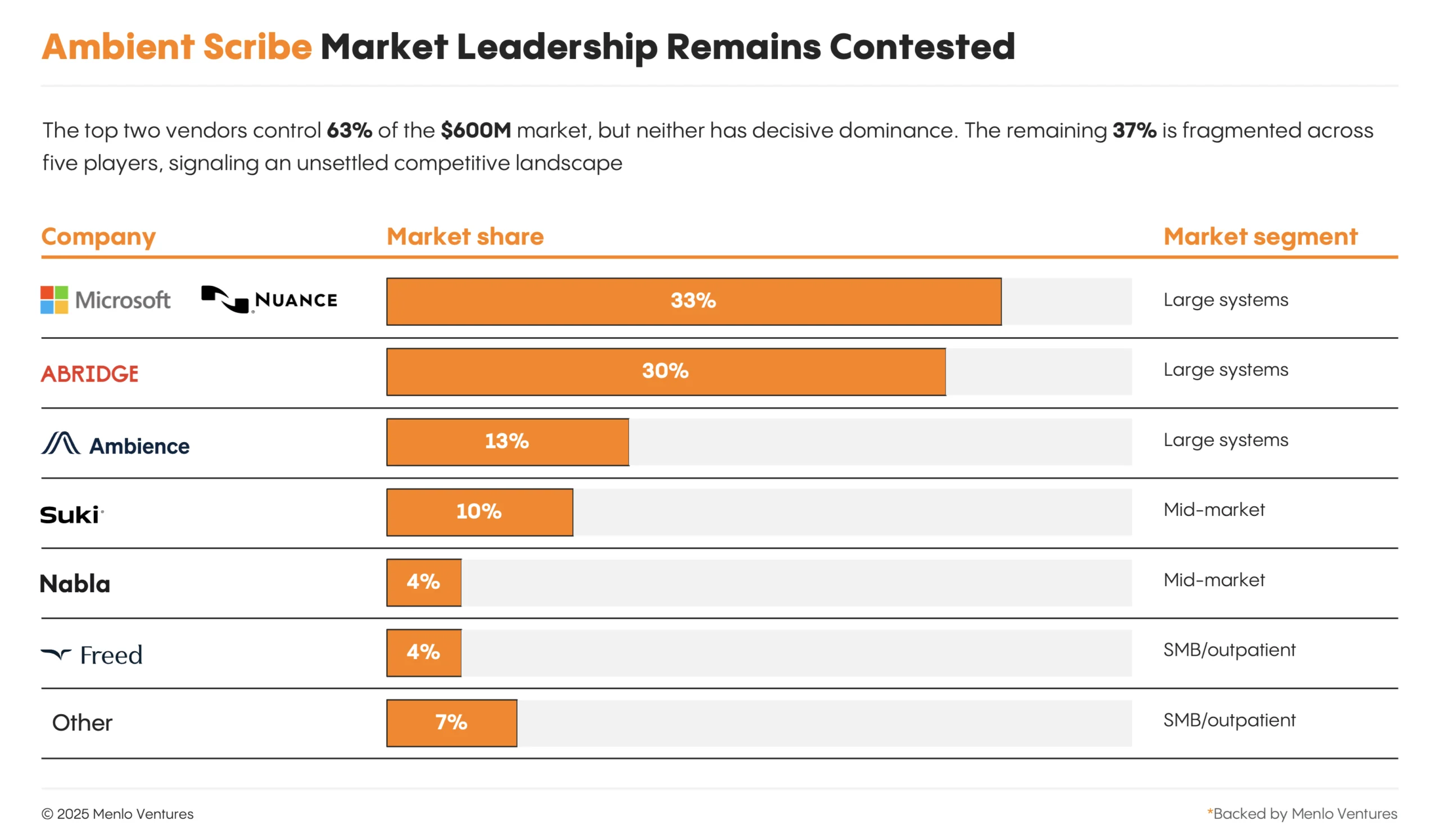

Bonus chart. Here’s the closest we’ll ever get to official ambient AI market share [Chart 4].

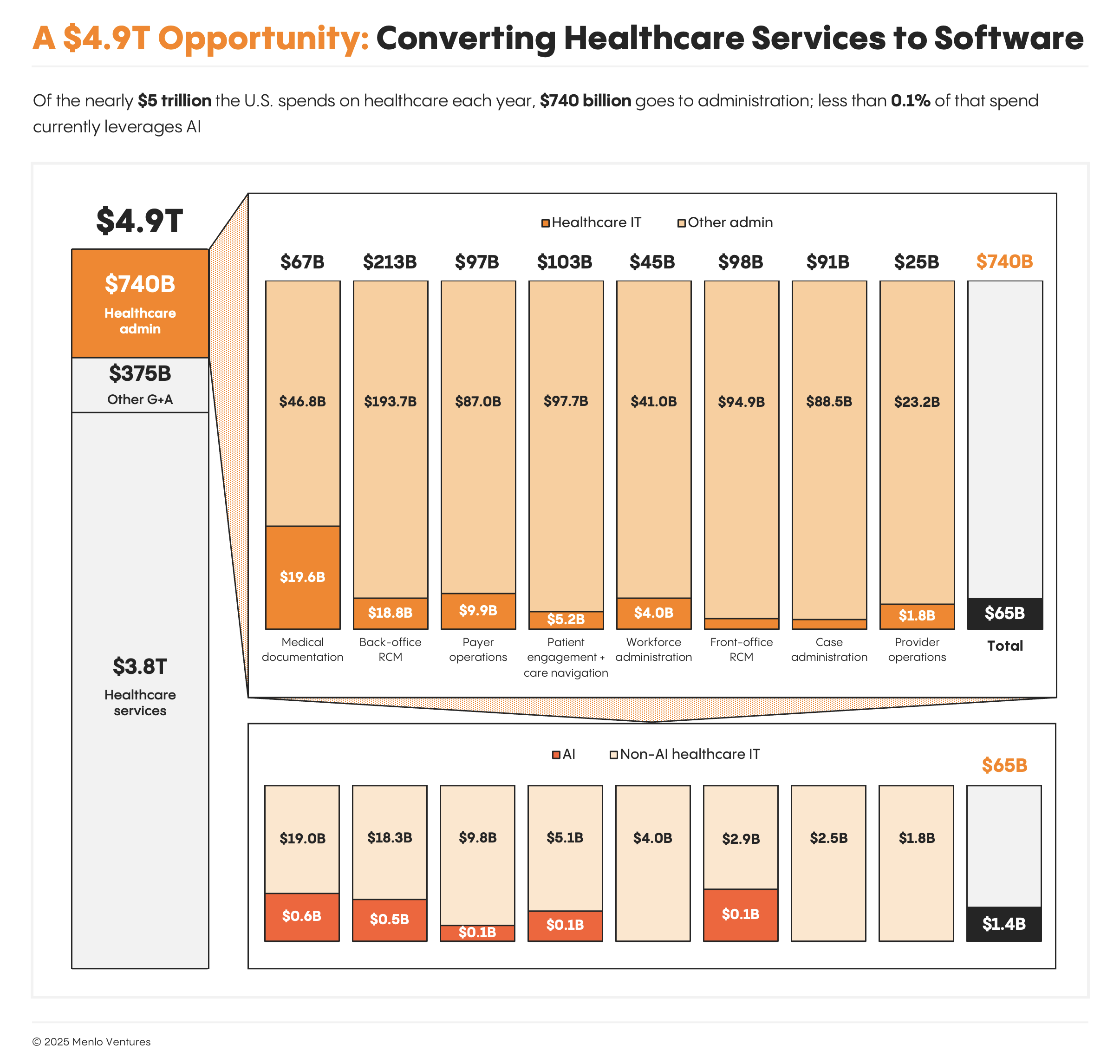

IT is good, services are great. Total U.S. healthcare administration spending reaches $740B annually, yet IT spend represents <10% of that. The report has a top tier breakdown [Chart 5].

- AI’s frontrunners found success carving into existing IT budgets, but the future victors could be the teams that convert services dollars into software dollars for the first time.

- AI offers the ability to automate workflows that have always been “people-intensive” – prior auth, patient engagement, front-office RCM – and Menlo believes 80% of this market is still completely untapped.

The Takeaway

Healthcare’s AI moment is here, and most of its potential has hardly been touched.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}