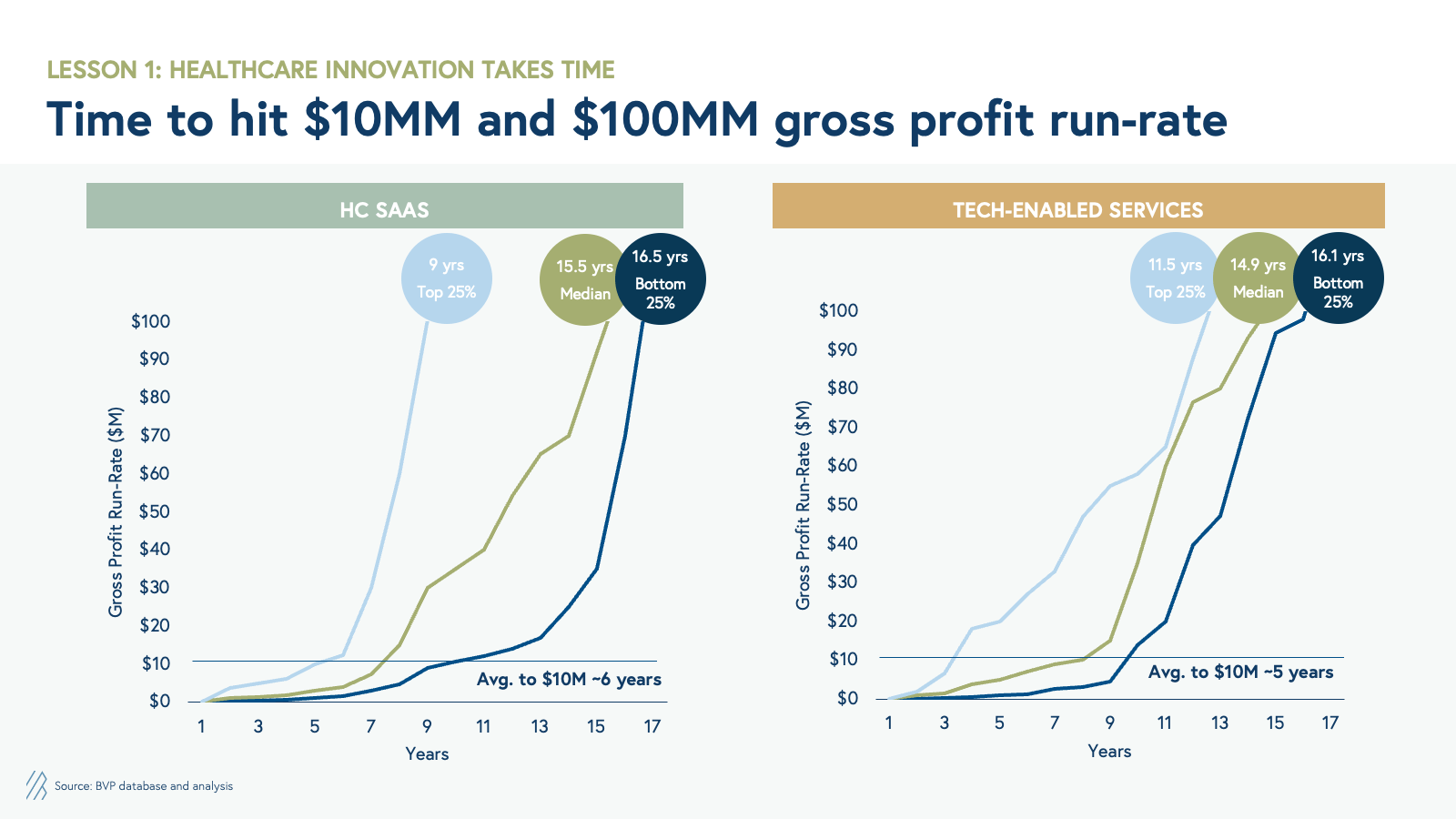

Bessemer Venture Partners’ always-stellar State of Healthcare AI report did a great job explaining why we (probably) aren’t in a bubble even though the health AI rocket has hit escape velocity.

AI is more than hype. BVP points to signals from the private markets to make its case.

M&A activity is surging. Global health tech M&A reached 400 deals in 2025 (up from 350 in 2024), but the strategic rationale matters more than the volume. Healthcare orgs and investors recognize that AI simultaneously drives revenue growth and margin improvement.

- Prime example: the Smarter Technologies roll up was designed to leverage Thoughtful and SmarterDx’s growth engine and clinical AI platform to drive margin expansion across the Access Healthcare RCM services conglomerate.

VC funding is nearly back to pandemic levels. BVP counted 527 venture deals in 2025 (~$14B total), with the average round size climbing 42% to $29M.

- AI startups captured 55% of that, up from 37% in 2024. Even more importantly, for every $1 invested in AI companies overall, $0.22 was deployed to healthcare AI startups, outpacing the fair share of 18% of GDP that healthcare spending represents in the U.S.

The question now is, are we in a bubble? BVP has a nuanced answer for why health AI is in a better spot than the Dot Com Bubble.

- First, AI’s technological shift has spurred the invention of new business models, with the emergence of “AI-services-as-software” companies delivering service-level outcomes (human-quality work) with software-level margins (70%+ gross margins).

- Second, buyers are now pulling instead of being pushed. While EHRs took 15 years to scale, AI scribes have pulled it off in three. Demonstrable ROI and ease of implementation were key here.

Health AI has an X Factor. New health AI “supernova” startups are bending traditional growth curves entirely. BVP attributes these supernovas’ unprecedented growth to four X Factors.

- Continuous hyper-growth velocity (not just growth projections)

- Revenue durability through defensibility

- Productivity gains that translate to better margins and full-time employee metrics at scale

- Point solution to platform expansion

Maybe sane valuations, maybe VC mental gymnastics. BVP argues that a supernova with $30M ARR and $1B valuation isn’t overvalued, it has fundamentally different growth dynamics.

- When you’re growing 6x instead of 2x, you reach $100M ARR in 18 months instead of 36+ months. That compression in time-to-scale commands a premium, and BVP says a 7x revenue multiple for supernovas is justified versus 2-3x for a strong SaaS company.

The Takeaway

Health AI is going supernova, and the explosion might actually be big enough to let the leaders grow into their astronomical valuations.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}