The ocean of digital health innovation seems to have a wave of new trends breaking every year, which is why Rock Health teamed up with LG NOVA to give enterprises a framework for “discerning promising currents from passing swells.”

Riding the wrong hype cycle can strain health systems’ limited resources with costly implementations or investment mistakes, so Rock Health divided the digital health landscape into 50 segments to see which show the most promise based on:

- Value potential (VP) – share of total digital health venture funding, disease burden (degree of economic cost), and addressable population size.

- Capturable opportunity (CO) – funding velocity, funding concentration (share of capital already held by large companies), and market maturity.

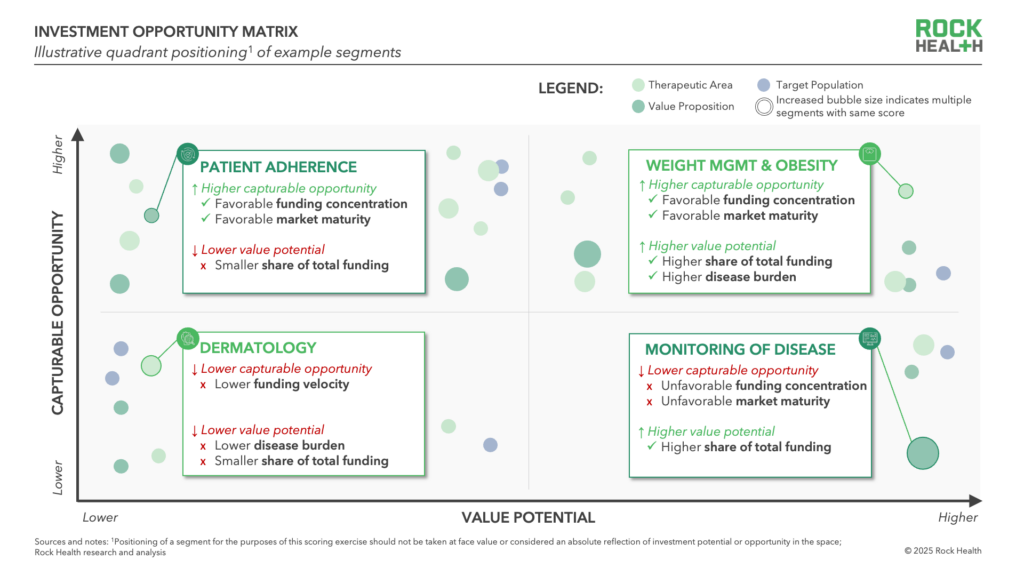

The “Goldilocks” waves include segments that are big enough to support a large market and ripe enough (but not too ripe) for new entrants to gain traction. [Chart: Strongest DH Segments]

- High VP, High CO: Weight Management stood out with the highest scores in both VP and CO. The disease burden and funding levels don’t get much higher, and the balance of early- and late-stage companies signals a strong market with room for new entrants.

- Low VP, High CO: Patient Adherence was docked for its smaller share of overall digital health funding, but stood out for its favorable funding concentration and market maturity.

- High VP, Low CO: Disease Monitoring had the opposite mix. The segment enjoys a large slice of the funding pie, but most of that is getting eaten by a few mega companies.

- Low VP, Low CO: Dermatology received the low marks across the board, with poor scores for funding velocity, disease burden, and overall share of funding.

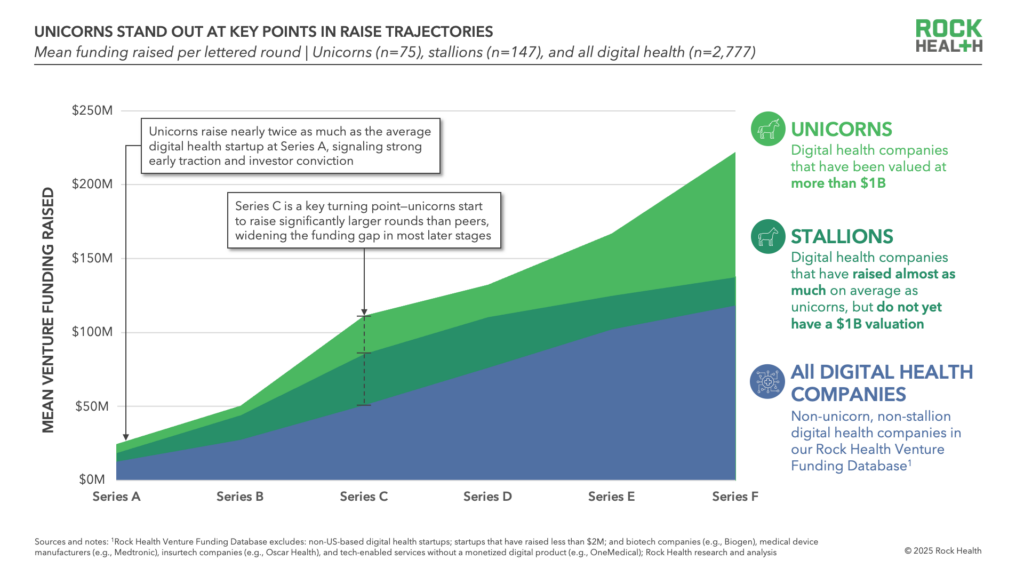

To complement its framework, Rock Health analyzed over 70 digital health unicorns to find other success signals from waves that the industry is already riding. Unicorns tended to:

- separate from the herd with larger Series C rounds (ex. Abridge)

- support care delivery or access and are often consumer-facing (ex. Wheel)

- be therapeutic area agnostic w/ broad addressable markets (ex. Included Health)

The Takeaway

Timing the digital health market is no small feat, but Rock Health’s framework provides a helpful tool for those looking to catch the best wave with their investments and implementations.

{kind=link}

{kind=link}

![[Chart 1]](https://research-assets.cbinsights.com/2025/04/16173953/SoDH-Q125-TLDR1-768x768.png){kind=link}

![[Chart 2]](https://research-assets.cbinsights.com/2025/04/16174019/SoDH-Q125-TLDR3.png){kind=link}

![[Chart 3]](https://research-assets.cbinsights.com/2025/04/16174031/SoDH-Q125-TLDR4.png){kind=link}

![[Chart 4]](https://research-assets.cbinsights.com/2025/04/16174049/SoDH-Q125-TLDR5.png){kind=link}