Rock Health’s industry analysis is a frequent feature in our top stories, but it’s tough to stay away with reports as consistently solid as last week’s 2023 Digital Health Startup Benchmarking Survey.

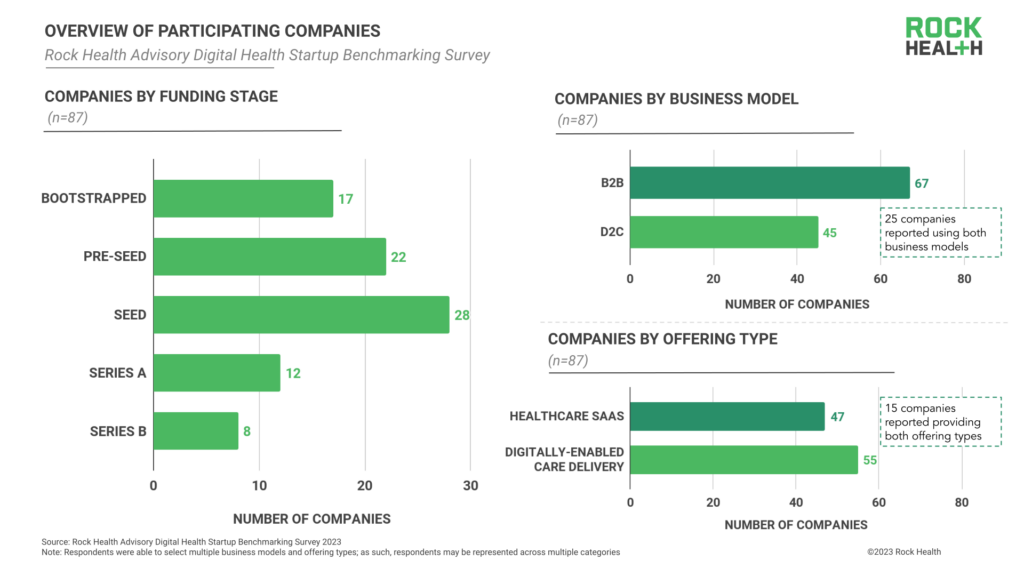

The survey broke down responses from 87 early-stage digital health startups to provide performance benchmarks for customer acquisition cost, lifetime value, expenses, and more [Chart: Company Breakdown by Stage / Segment].

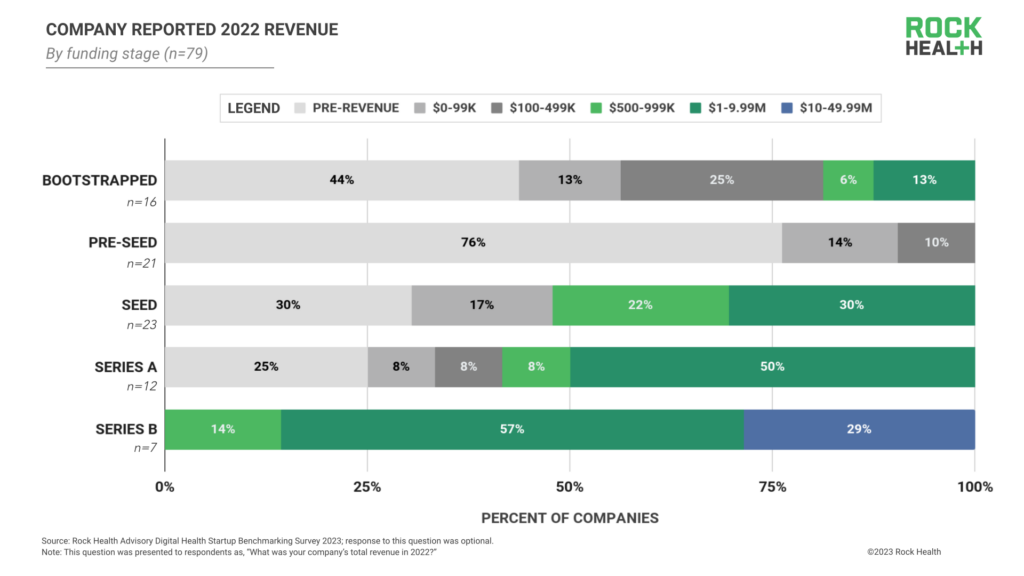

Series B is a tipping point for growth, but not (yet) margins.

- [Chart: Revenue by Funding Stage] While Series A startups are generally building an MVP and testing product-market fit, no Series B respondents were still pre-revenue (vs. 25% of Series A). That revenue is going straight to growth, with just 12% of Series B startups reporting positive margins (a small increase from 9% of Series A).

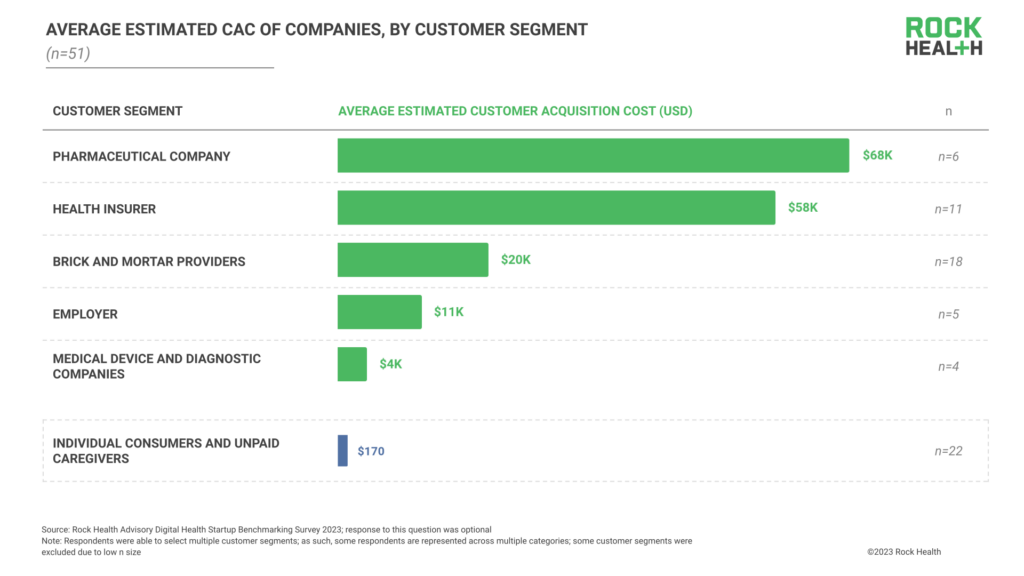

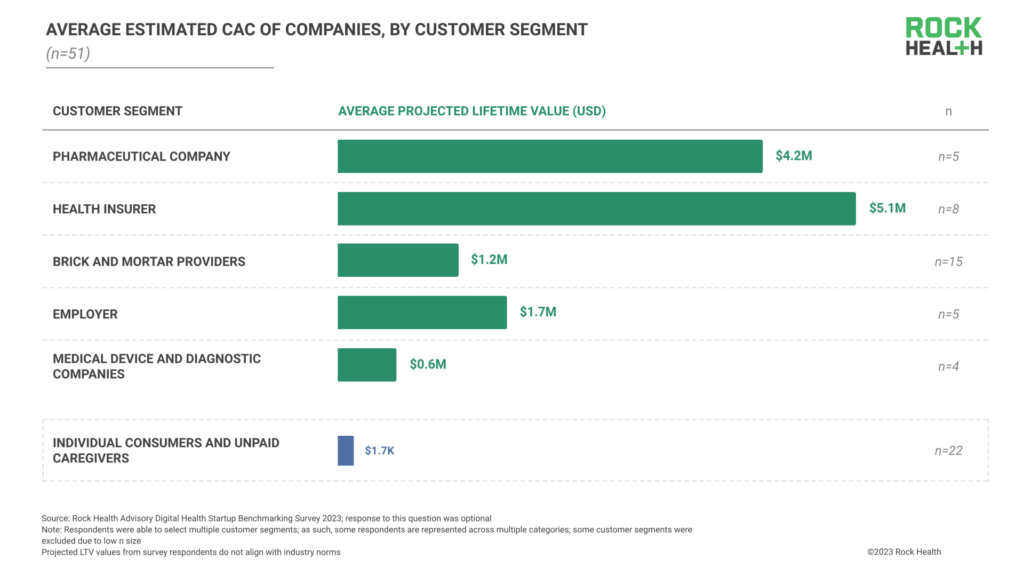

CAC and LTV calculations are challenging for early-stage startups.

- [Chart: CAC by Customer Segment][Chart: LTV by Customer Segment] Both CAC and LTV vary widely by customer type, but both charts illustrate that “you get out what you put in.” It cost respondents an average of $58k to sign a payor, but the average lifetime value was $5.1M. That compares to a CAC of $170 and an LTV of $1.7k for consumers.

Engagement metrics are the first step to robust outcomes.

- On average, each company reported tracking two engagement outcome metrics, two clinical outcome metrics, and one economic outcome metric. “For startups balancing speed-to-outcomes and quality-of-outcomes, an ‘engagement first, clinical/economic later’ approach might help to toe the line.”

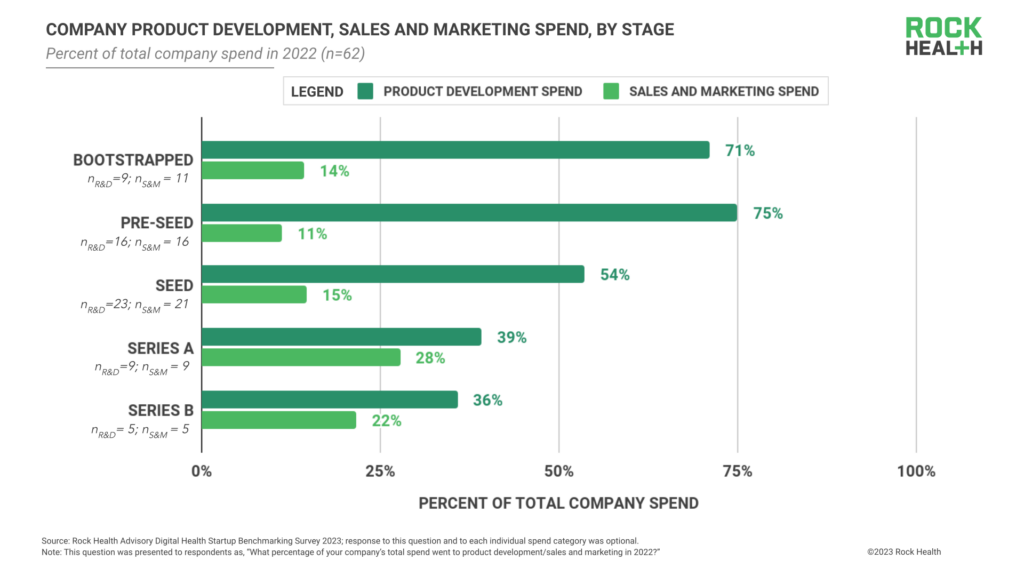

Navigating product versus marketing costs is a balancing act.

- [Chart: Company Product vs. Marketing Costs] The amount of revenue the startups devote to product versus business development and marketing evolves alongside scale. Pre-seed respondents allocated 75% of revenue to product and 11% to marketing, while Series B respondents allocated 36% of revenue to product and 22% to marketing.

The Takeaway

We’re lucky to be in a golden age of startup transparency, and between this Rock Health survey and the latest State of CareOps report, there’s no shortage of great information out there for founders to use as guideposts in their pursuit of scale.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}