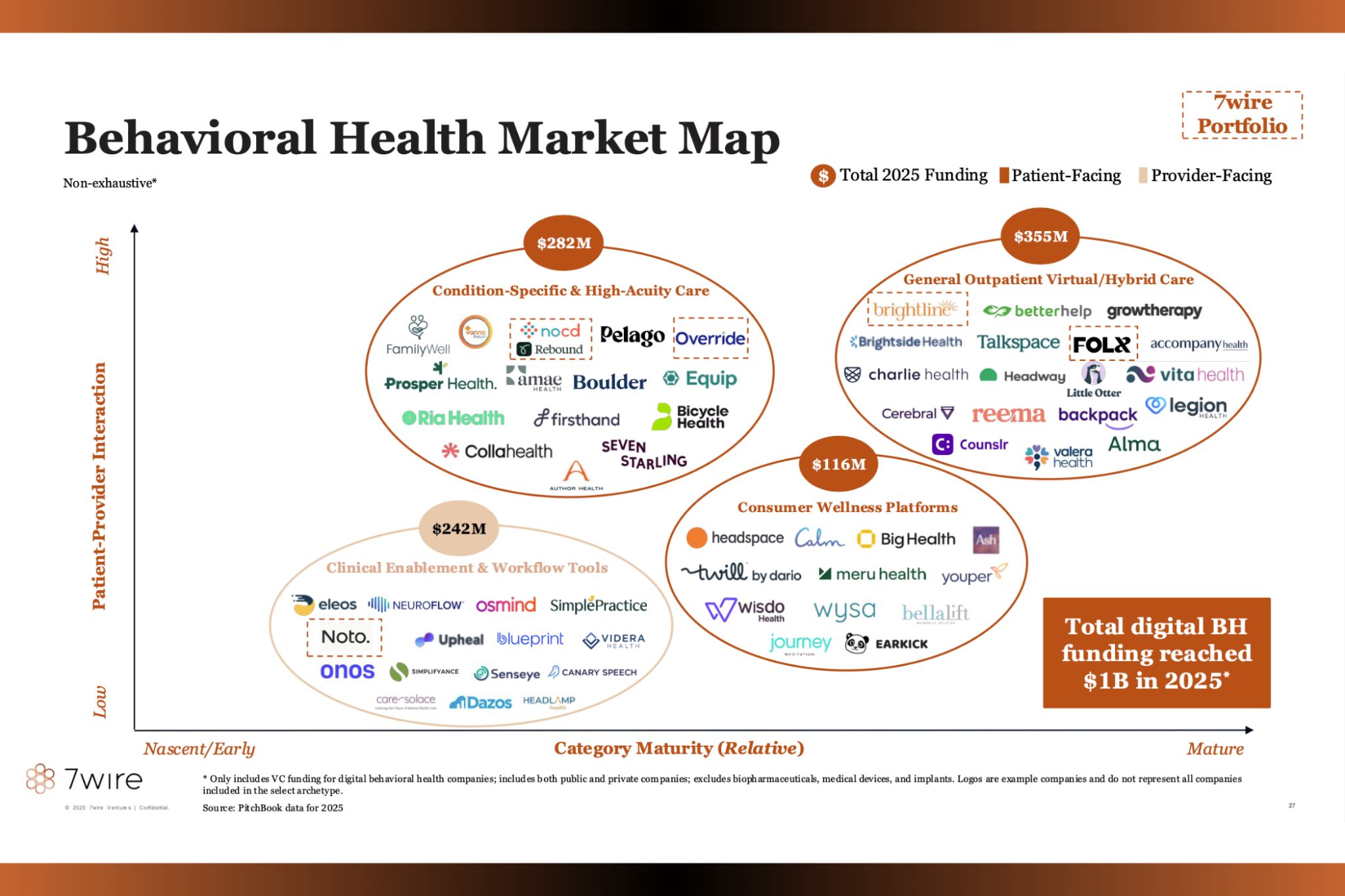

Although we touched on Walmart’s rumored acquisition of ChenMed last week, the ongoing talks are continuing to drum up lots of conversation around the healthcare strategy of major retailers and the potential implications if the deal goes through.

Here’s a quick primer on Walmart’s healthcare strategy, which so-far can be bucketed into three themes: Medicare and MA health plans, primary care, and employer virtual care.

- Back in 2018, Walmart looked into making one of the grandest entrances to the market imaginable with a $67B acquisition of Humana. When that didn’t materialize, it pursued a more balance-sheet-friendly approach by launching its own in-house Medicare and MA plans, as well as partnering with UnitedHealth on a co-branded MA plan.

- Walmart Health then debuted in 2019, and it’s a more comprehensive offering than it seems to get credit for. The 30 current locations provide primary care, urgent care, labs, imaging, optometry, audiology, and even dentistry.

- When Walmart scooped up telehealth provider MeMD in 2021, it began offering virtual primary care and behavioral healthcare through commercial payors and employers.

Enter ChenMed, a senior-focused primary care provider with over 125 clinics across 15 states, making it the last major M&A target in the space following CVS-Oak Street and Amazon-One Medical.

- ChenMed also takes on full-risk risk for the cost of its patients’ medical care, incentivizing long-term relationships and preventive care as opposed to the typical retail clinic model focused on episodic needs.

The acquisition would stake Walmart’s claim in the primary care land grab, allowing it to continue its push into the ever-growing Medicare Advantage market while leveraging ChenMed’s proven platform instead of building from the ground up.

- At one point, Walmart had ambitions to open 4,000 of its own clinics – plans that have since been scrapped – yet now only has four new locations planned for next year after a string of operating challenges caused it to pump the brakes.

- With some of Walmart’s largest competitors diving head first into care delivery, and limiting the options of late entrants in the process, the timing makes sense to either go all-in or risk losing ground to the competition.

The Takeaway

The number of attractive primary care clinic operators isn’t getting any bigger, and Walmart’s window of opportunity is shrinking if it wants to take the side door into the industry. There isn’t much of a ceiling on the splash that Walmart’s $600B in annual revenue and 4,300 retail locations could make in healthcare, especially if it can pick up an operator like ChenMed with the expertise and track record to help pull it off.